.jpeg)

.svg)

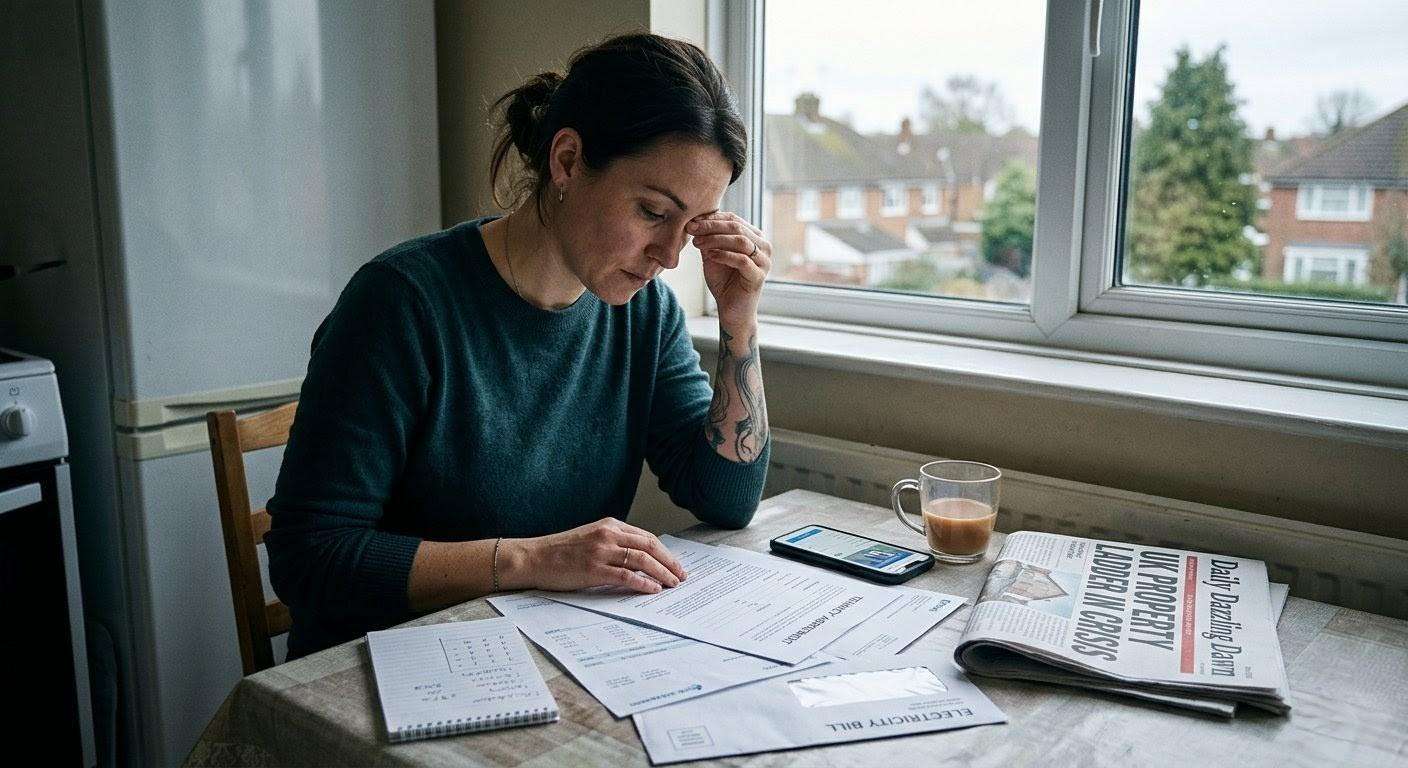

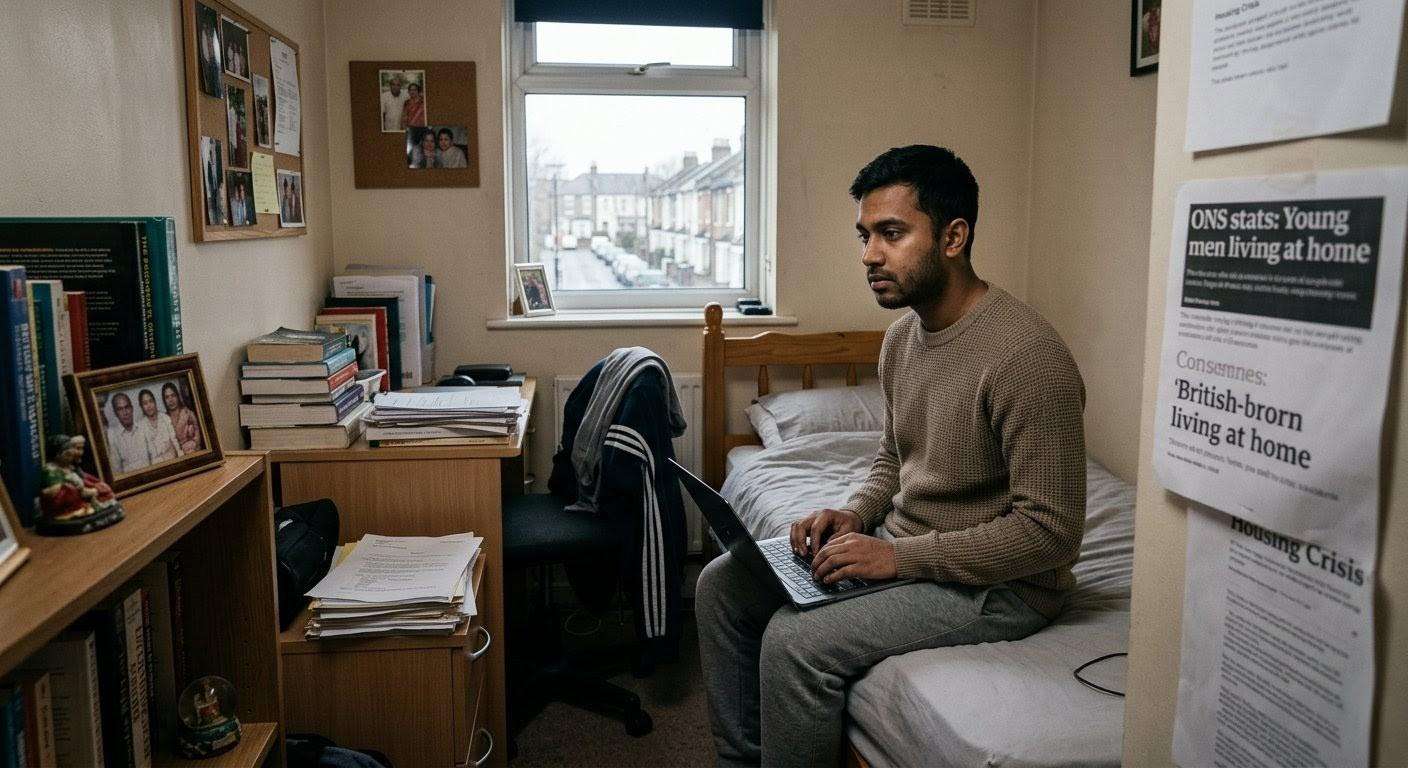

The United Kingdom's protracted housing crisis shows little sign of abating, remaining a significant drag on the national economy. Despite recent governmental efforts and policy tweaks, the core problems of unaffordable house prices and stagnant wages persist, leaving experts and hopeful homeowners with the bleak assessment that a rapid fix is simply not on the horizon.

Chancellor Rachel Reeves's latest attempts to invigorate the market through changes to mortgage lending, designed to offer more credit to lower-income first-time buyers, have been met with skepticism. Vicky Spratt, Housing Correspondent for The i Paper, observes that such measures often merely inflate house prices further, trapping prospective homeowners in a cycle of ever-increasing debt. This continuous feedback loop has pushed the dream of homeownership beyond the reach of many, particularly younger generations, with property values in some areas now commanding an astonishing eight, nine, or even ten times the average wage.

From within the Bank of England, Senior Economist Rupal Patel sheds light on the delicate balancing act performed by the Monetary Policy Committee (MPC) when setting interest rates. While the peak inflation of 11% in 2022 was a critical concern, the opposite extreme of deflation would be equally detrimental to the economy. The current Bank Rate of 4.25% reflects this precarious equilibrium, aiming to steer inflation back towards its 2% target without stifling economic activity. However, Patel frankly admits that the Bank's influence over the intricacies of the private housing market is inherently limited.

The harsh reality, a consensus among economists and government advisors, is that straightforward solutions are few and far between. Patel underscores this point, stating, "Because the housing market is a private market, there are few things that the Bank of England or even really the Government can do to make housing more affordable." Without substantial government intervention, such as the direct provision of genuinely affordable housing or significant subsidies for homeownership – akin to past schemes like Help to Buy – the deeply ingrained issues are expected to endure. The critical question facing the new Labour Government is whether they possess the political will to enact truly transformative, and potentially unpopular, measures.

Latest Developments Offer Glimmers, But No Guarantee

While the immediate outlook remains challenging, recent government announcements and market shifts offer some context to the ongoing crisis. The Labour Government has unveiled a substantial housing renewal initiative as part of their "Plan for Change." This includes a £39 billion Social and Affordable Homes Programme over the next decade (2026-27 to 2035-36), targeting the delivery of 300,000 new social and affordable homes, with a significant proportion (at least 60%) allocated for social rent – a sixfold increase compared to the previous decade. Overall housing targets have also been raised to 1.85 million new homes within the first five years.

Is the UK Property Dream Dead?

Furthermore, Labour is set to reform the Right to Buy scheme. These reforms aim to lengthen the eligibility period for tenants to purchase their social home from three to ten years, reduce the discount offered, and exempt all newly built social homes from being sold off via Right to Buy for 35 years. Local authorities will also be permitted to retain 100% of their Right to Buy receipts for reinvestment in new housing.

Beyond these policy shifts, the "Delivering a Decade of Renewal for Social and Affordable Housing" strategy emphasizes improving housing quality and safety, modernizing the Decent Homes Standard to include private rentals, and introducing Minimum Energy Efficiency Standards in social housing. "Awaab's Law," set to come into force in 2025, will mandate swift action on hazards like damp and mould. Complementing these efforts, the government has announced a £20 million investment in community-led housing initiatives.

In the broader economic landscape, the Bank of England has maintained its base rate at 4.25% as of June 2025, though analysts widely anticipate further cuts later in the year, potentially bringing the rate down to 3.75% by year-end, which could offer some relief on mortgage rates. Despite the persistent challenges, house price predictions for 2025 suggest continued, albeit modest, growth, ranging from 2% to 4%, influenced by potential interest rate adjustments, wider economic conditions, and the impact of evolving government policy.